The Federal election is coming up this fall which means the office in power has released its proposed 2019 budget. It includes several bits of bait to encourage re-election, including two incentives for first-time home buyers.

The first lure is a change to the existing Home Buyers Plan (HBP.) This program allows first-time home buyers can borrow money from their RRSPs to use as a down payment. Presently the limit is $25,000 but the proposal states this will be increased to $35,000.

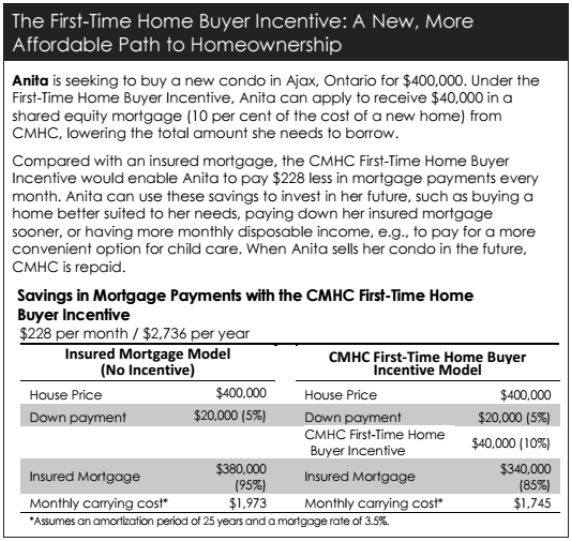

CMHC First-Time Home Buyers Incentive

The second lure is a little more enticing. It’s better understood as a “shared equity mortgage.” This means that the Canadian Mortgage and Housing Cooperation (CMHC) will loan you some money to pay for your home and you’ll pay it back out of the equity you earn after you sell the property. You still have to come up with the initial 5% down payment but then the government will give you an additional 5% (for resale homes) or 10% (for new builds.)

How will this make a difference in the every-day life of a home buyer? Lets compare using the example given in the 2019 proposed budget.

In this example we see that the home buyer, Anita, provided her own 5% down payment and then received a 10% incentive from the program, which thereby decreased her monthly mortgage payment by $228. This savings may be all she needs in order to afford her first home. Or, it may be extra money she can use toward other life goals, investments, or additional payments toward her mortgage. The choice is hers.

Limited borrowing power

This proposed incentive may have many potential first-time buyers grinning from ear to ear, but it should be noted that within the program, your borrowing power will be less. “The current qualifying criteria, including the stress test, allows a household to qualify for a house that is 4.5-4.7 times their household income,” James Laird, president of CanWise Financial, said. Not only will the CMHC incentive be restricted to those with an annual household income of $120,000 or less, but the participant’s insured mortgage and incentive amount will have a maximum amount of 4 times the annual household income. This means that a household making $120,000 a year could qualify outside the program for a home priced at a maximum of $564,000. But inside the program the same household would only qualify for a home priced at a maximum of $480,000. The borrowing power shrinks by 15%.

Specific details on the program will become available after the federal election in the fall if the present office is re-elected. Until then, take a minute to find out how much mortgage you could qualify for by using our pre-approval application below, or contact us directly.

[ApplicationFormv1.1]